Why buy life insurance? Secure your family's future

- JF Strawderman

- Apr 10

- 8 min read

TL;DR:

Many U.S. families are underinsured, often carrying only 1 to 3.5 times their income instead of the recommended 10 to 15 times. Most coverage gaps average $320,000, putting families at financial risk if a primary earner passes away. Life insurance benefits go beyond funeral costs, including income replacement, mortgage payoff, debt clearance, and funding education, while often being tax-free.

Most U.S. families believe they have enough life insurance. They don’t. 44% of households admit they feel underprotected, and the typical family carries only 1 to 3.5 times their annual income in coverage when financial experts recommend 10 to 15 times. That gap is not a minor miscalculation. It can mean the difference between your family maintaining their home and lifestyle or scrambling to cover basic bills within months of losing you. This guide breaks down why life insurance matters, what it actually covers, how to calculate the right amount, and how it fits into a broader financial plan.

Table of Contents

Key Takeaways

Point | Details |

Most families underinsured | U.S. families on average have much less life insurance than experts recommend, leaving costly financial gaps. |

Covers more than funerals | Life insurance replaces lost income, covers debts, and provides for loved ones—not just funeral costs. |

Calculate needs carefully | Use methods like the DIME formula and 10–15x income rule to decide on the right coverage. |

Employer plans rarely enough | Relying solely on group policies often leaves families underprotected. |

Secure peace of mind | Buying appropriate life insurance delivers lasting peace of mind for you and your dependents. |

Why most U.S. families are underinsured

The numbers are sobering. The average coverage gap in U.S. families sits at $320,000, meaning most households are carrying far less protection than they actually need. Young families are hit hardest because they tend to have higher debt, lower savings, and more dependents relying on their income.

A big part of the problem is misplaced confidence in workplace benefits. Employer-provided group life insurance typically covers only 1 to 2 times your annual salary. If you earn $75,000 per year, that means your family might receive $75,000 to $150,000 when they need closer to $750,000 to $1,125,000 to maintain financial stability. That shortfall is enormous.

Here is why family insurance coverage gaps are so common:

Reliance on employer plans that end the moment you change jobs or get laid off

Underestimating real costs like childcare, college tuition, and long-term debt

Assuming coverage is too expensive when term life insurance can cost less than a streaming subscription per month

Delaying the decision until health issues make coverage harder or more costly to obtain

When you compare life insurance policies side by side, the difference between what employer plans offer and what a personal policy provides becomes very clear, very fast.

Pro Tip: Never treat your employer’s group life insurance as your primary coverage. It’s a starting point, not a solution. Build a personal policy around it so your family stays protected no matter what happens to your job.

The reality is that most families don’t realize they’re underinsured until it’s too late. Reviewing your coverage now, before a health change or life event, gives you the most options and the best rates.

What life insurance actually covers

Most people think life insurance is for covering funeral costs. That’s only a small piece of what it does. The median funeral cost is $8,300 for burial or $6,280 for cremation. A well-structured policy does far more than cover that.

Here is what a death benefit can actually pay for:

Income replacement so your family can maintain their standard of living for years

Mortgage payoff to keep your family in their home

Consumer debt including car loans, credit cards, and student loans

Childcare and household services especially if a stay-at-home parent passes away

College tuition for children who are years away from graduating

Final medical expenses that insurance may not fully cover

One thing many families don’t realize is that the death benefit is received income-tax-free by your beneficiaries. In 2026, tax-free death benefits can be passed on with estate tax exemptions up to $13.99 million, making life insurance one of the most efficient wealth transfer tools available.

Coverage need | What life insurance can do |

Lost income | Replace years of earnings for dependents |

Mortgage | Pay off remaining balance |

Childcare | Fund ongoing care costs |

Education | Cover tuition and related expenses |

Debt | Eliminate loans and credit balances |

Funeral costs | Cover burial or cremation expenses |

Modern policies have also evolved. Many now include living benefits, which allow you to access a portion of your death benefit while still alive if you’re diagnosed with a chronic or terminal illness. This feature can be a financial lifeline when medical bills pile up.

“Life insurance is not just about dying. It’s about making sure the people you love can keep living the life you built together.”

Stay-at-home parents are often overlooked in coverage conversations. Replacing the services they provide, including childcare, cooking, transportation, and household management, carries real financial cost. Understanding how life insurance works for every member of your household helps you avoid dangerous blind spots.

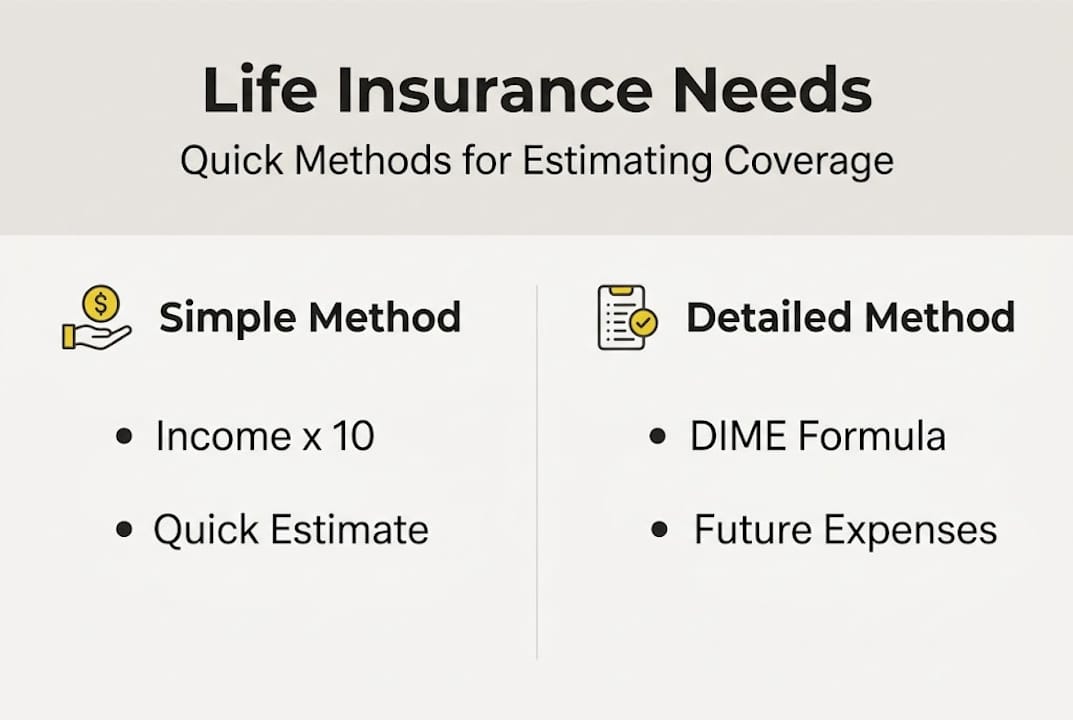

How to calculate your life insurance needs

Guessing at a coverage number is one of the most common mistakes families make. There are two reliable methods to get to the right figure.

Method 1: The income multiplier Multiply your annual income by 10 to 15. This gives you a fast baseline. If you earn $80,000 per year, you need between $800,000 and $1.2 million in coverage.

Method 2: The DIME method The DIME method is more precise. It stands for:

Debt: Add up all personal debts excluding your mortgage

Income: Multiply your annual income by the number of years your family needs support

Mortgage: Include your full remaining mortgage balance

Education: Estimate college costs for each child

Then subtract any existing assets or savings. The result is your target coverage number.

For families with a stay-at-home parent, don’t forget to factor in replacement costs. The average cost to replace a stay-at-home parent’s services is $17,836 per child per year. Over 10 years with two children, that’s more than $350,000 in services alone.

Method | Best for | Complexity |

Income multiplier | Quick estimate | Low |

DIME method | Accurate planning | Medium |

Needs analysis with advisor | Customized precision | High |

Also account for inflation. A policy that feels adequate today may fall short in 15 years as costs rise. Building wealth with insurance means thinking long-term, not just covering today’s expenses.

Pro Tip: Consider laddering your policies. For example, buy a 30-year term for your mortgage and a 20-year term for income replacement. As your needs shrink over time, your premiums do too.

The goal is not to over-insure. It’s to be precise. A thoughtful calculation today prevents your family from being left with too little when it matters most.

Life insurance as part of your financial plan

Life insurance is not a savings account. It’s not an investment vehicle. It’s a risk management tool, and understanding that distinction changes how you use it.

For most families, the smartest approach is term life insurance combined with disciplined investing. Wealthier households buy more insurance even after controlling for need, but research consistently shows that term life insurance is the most cost-effective solution for the majority of families.

Here is how life insurance fits alongside your other financial tools:

Emergency fund: Covers short-term gaps; life insurance covers long-term income loss

Retirement accounts: Build wealth over time; life insurance protects the people depending on that wealth

Home equity: Valuable but illiquid; life insurance provides immediate cash to beneficiaries

Social Security survivor benefits: Helpful but limited; rarely enough to replace full income

Permanent life insurance, such as whole life or universal life, does build cash value over time. But the returns are typically lower than what you’d earn through a diversified investment portfolio. Don’t buy permanent life insurance as an alternative to investing. Buy it if you have a specific need for lifelong coverage or estate planning.

Life insurance also plays a role in retirement and estate planning. It can provide liquidity to cover estate taxes, equalize inheritances among heirs, or fund a trust for a dependent with special needs. These are strategic uses that go well beyond basic income replacement.

Pro Tip: Review your coverage every three to five years or after any major life event, including marriage, a new child, a home purchase, or a significant income change. Your needs evolve, and your policy should too.

The families who benefit most from life insurance are those who treat it as a deliberate part of their financial plan, not an afterthought.

A fresh perspective: What most families miss about life insurance

Here’s something worth saying plainly: the most powerful thing life insurance does is not pay for a funeral or build cash value. It buys your family time. Time to grieve without financial panic. Time to make good decisions instead of desperate ones. Time to keep the kids in the same school, stay in the same house, and maintain some sense of normal.

The biggest regrets we see in claims situations come from two places. First, families who let coverage lapse or never updated it after a major life change. Second, families who relied entirely on a workplace plan that disappeared when the job did.

Most people don’t need a complicated policy. They need the right amount of coverage, reviewed regularly, and structured to match their actual life. Why safeguarding your family’s future matters is not about fear. It’s about being the kind of person who plans ahead so the people you love never have to face the worst day of their lives and a financial crisis at the same time.

True security is not about the type of policy you own. It’s about having enough coverage, at the right time, for the right reasons.

Take the next step toward protecting your family

You now understand the coverage gap, what life insurance really does, how to calculate what you need, and how it fits into your financial life. The next step is making it real for your specific situation.

At Strawderman Financial, we work with families across the U.S. to find coverage that fits their lives and their budgets. Whether you’re looking to explore life insurance options for the first time or want to revisit your current plan, our agents offer free consultations with no pressure. We also provide financial planning help for retirement and estate needs. Let’s make sure your family is protected the right way.

Frequently asked questions

What is the main reason to buy life insurance?

The core reason is to provide a financial safety net for your loved ones if you pass away, ensuring they aren’t burdened by lost income or unexpected expenses. For most families, term life insurance is the most practical and affordable way to do that.

How much life insurance should I buy?

Experts recommend 10 to 15 times your annual income, and the DIME method gives you a more precise number by factoring in debt, income replacement, mortgage balance, and education costs minus your existing assets.

Is employer-provided life insurance enough?

Employer plans cover only 1 to 2 times your salary, which falls far short of the 10 to 15 times most families need. A personal policy ensures your coverage stays with you regardless of your employment status.

Are life insurance payouts taxable?

In almost all cases, death benefits are received income-tax-free by beneficiaries. In 2026, estate tax exemptions allow up to $13.99 million to pass tax-free, making life insurance one of the most efficient ways to transfer wealth.

Does life insurance cover stay-at-home parents?

Absolutely. Coverage can replace the value of childcare and household services, which average over $17,836 per child annually. That cost adds up quickly and should be factored into any family’s coverage calculation.

Recommended

Comments