Health insurance terms explained: A clear family guide

- JF Strawderman

- Apr 15

- 8 min read

TL;DR:

Health insurance terminology can be confusing, causing costly mistakes without proper understanding.

Understanding key terms like premium, deductible, copay, and out-of-pocket max helps in choosing the right plan.

Regularly reviewing and comparing plan details ensures coverage aligns with your family’s changing needs and finances.

Open enrollment arrives, and suddenly you’re staring at a wall of words: premium, deductible, coinsurance, out-of-pocket maximum. Your family’s health and your household budget both hang on understanding what these mean, yet the paperwork reads like a foreign language. Choosing the wrong plan because of a misunderstood term can cost thousands of dollars. This guide cuts through the noise. We’ll define every critical term in plain English, show you how plan tiers affect real costs, and give you a practical framework for making smarter coverage decisions before you sign anything.

Table of Contents

Key Takeaways

Point | Details |

Decoding key terms | Understanding core insurance words helps prevent surprise costs and makes policy choices easier. |

Plan tier impacts | Choosing the right metal tier and subsidy eligibility can significantly lower total expenses. |

Budget with max limits | Knowing your out-of-pocket maximum lets you budget for a worst-case scenario and avoid major debt. |

Use terms strategically | Applying what terms mean to your real-life needs helps you pick and use the best plan for your family. |

Why health insurance language feels overwhelming

Most people only engage with health insurance twice a year: during open enrollment and when something goes wrong. Neither moment is exactly calm. You’re either racing a deadline or dealing with a health scare, and in both cases, confusing paperwork is the last thing you need.

The terminology itself is part of the problem. Words like “coinsurance” and “copay” sound similar but work very differently. “In-network” and “out-of-network” sound straightforward until you realize your preferred doctor may fall into either category depending on your plan. And terms like “Explanation of Benefits” (EOB) don’t explain much at all when you first see one.

Here’s what makes it worse: insurance documents are not written for you. They’re written to satisfy legal and regulatory requirements. That means dense language, fine print, and definitions buried in appendices. Even people who work in finance sometimes struggle to decode a Summary of Benefits and Coverage (SBC) on the first read.

Knowing what is health insurance at a foundational level is the starting point, but the real decisions happen at the term level. Here’s a snapshot of what trips people up most:

Premium vs. deductible: Many people focus only on the monthly premium and ignore the deductible, which can be thousands of dollars.

Copay vs. coinsurance: A copay is a flat fee; coinsurance is a percentage. Mixing them up leads to budget surprises.

Network restrictions: Choosing an out-of-network provider by accident can result in bills your insurance won’t cover.

EOB misread as a bill: Many families panic when they receive an EOB, not realizing it’s a summary, not an invoice.

“Cost Sharing Reductions (CSR) are subsidies available for Silver plans that reduce deductibles and copays for individuals and families earning between 100% and 250% of the federal poverty level, yet millions of eligible families never claim them.”

That last point is critical. Confusion about terms doesn’t just cause stress. It causes people to leave real money on the table.

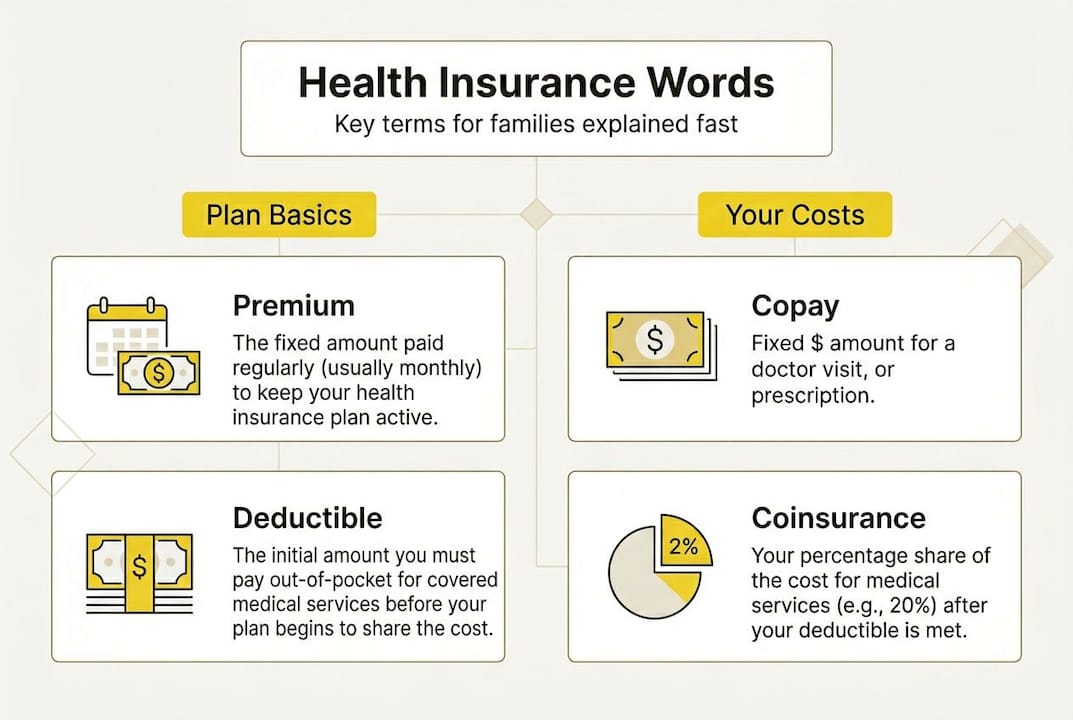

The health insurance glossary: Essential terms explained

Now that we know why the terminology confuses, let’s make it simple. Below is a table of the most important terms you’ll encounter, with plain-language definitions and quick examples.

Term | Definition | Example |

Premium | Monthly payment to keep your plan active | $450/month regardless of whether you see a doctor |

Deductible | Amount you pay before insurance kicks in | You pay the first $1,500 of medical bills each year |

Copay | Flat fee for a specific service | $30 every time you visit your primary care doctor |

Coinsurance | Your percentage share after the deductible | You pay 20%, insurance pays 80% |

Out-of-pocket max | The most you’ll pay in a year | After $10,600, your insurer covers 100% |

Network | Doctors/hospitals contracted with your insurer | Seeing an in-network doctor costs less |

EOB | Summary of what was billed and what insurance paid | Not a bill; just a record of the transaction |

Formulary | List of drugs your plan covers | Generic drugs often cost less on the formulary |

For 2026, the ACA out-of-pocket max is $10,600 for individuals and $21,200 for families for in-network essential health benefits. Out-of-network costs can push those numbers higher.

Here’s how a claim actually moves through the system:

You receive a covered service from your doctor.

Your provider submits a claim to your insurance company.

The insurer checks whether the service is covered and whether the provider is in-network.

The insurer applies your deductible, then calculates your coinsurance or copay.

You receive an EOB showing what was billed, what insurance paid, and what you owe.

Your provider sends you a bill for your portion.

Understanding insurance types for 2026 also matters because HMOs, PPOs, and EPOs handle networks and referrals differently. And if you have a pre-existing condition, knowing how your plan handles it is essential before you enroll.

Pro Tip: The most overlooked cost is coinsurance after the deductible. People budget for the deductible but forget they still owe a percentage of every bill until they hit the out-of-pocket max. Check your SBC’s “What You Will Pay” column for each service type.

How plan tiers and subsidies affect real costs

Once terms are understood, the question becomes how they affect your wallet in practice. The ACA marketplace organizes plans into four metal tiers, each with a different balance between monthly premiums and out-of-pocket costs.

Tier | Avg. Monthly Premium | Avg. Deductible | Out-of-Pocket Max | Best For |

Bronze | Lowest | $6,000+ | Up to $10,600 | Healthy, low utilization |

Silver | Moderate | $3,000-$5,000 | Varies with CSR | Subsidy-eligible families |

Gold | Higher | $1,000-$2,000 | Lower | Regular care needs |

Platinum | Highest | Near $0 | Lowest | Chronic conditions, high use |

For healthy individuals, Bronze plans minimize costs when you rarely use medical services. If you expect frequent doctor visits, prescriptions, or procedures, Gold or Platinum plans often save money despite higher premiums. Silver is the strategic sweet spot for subsidy-eligible families because Cost Sharing Reductions apply only to Silver plans.

Here’s a quick look at common subsidies and who qualifies:

Premium Tax Credit (PTC): Reduces your monthly premium. Available to individuals and families earning between 100% and 400% of the federal poverty level.

Cost Sharing Reduction (CSR): Lowers your deductible, copay, and out-of-pocket max. Only available on Silver plans for those earning 100% to 250% of the federal poverty level.

Medicaid: Full coverage for those below 138% of the federal poverty level in expansion states.

CHIP: Low-cost coverage for children in families that earn too much for Medicaid but can’t afford private insurance.

The 2026 out-of-pocket maximum of $10,600 per individual is a useful planning number. Think of it as your worst-case annual healthcare cost. If you can cover that amount from savings or an HSA (Health Savings Account), a high-deductible Bronze plan may work well. If you can’t absorb that risk, a Gold plan’s higher premium may be the smarter trade.

When choosing a health plan, run the math both ways: add up 12 months of premiums plus your expected out-of-pocket costs under each tier. The plan with the lowest total annual cost for your actual usage pattern is usually the right one.

How to use insurance terms for smarter decisions

Armed with definitions and context, here’s how to use that knowledge when making choices. Understanding terms is only valuable if it changes how you act during enrollment and throughout the year.

Pull your Summary of Benefits and Coverage (SBC). Every plan must provide one. Read the “Important Questions” section first. It lists the deductible, out-of-pocket max, and whether you need referrals.

Map terms to your family’s actual needs. How many prescriptions does your family fill monthly? How often do you see specialists? Estimate your realistic annual usage before comparing plans.

Use the out-of-pocket max as your budget ceiling. The 2026 individual max of $10,600 is your worst-case number. Plan your emergency fund or HSA contributions around it.

Check subsidy eligibility before you pick a tier. If you qualify for CSR, a Silver plan will outperform a Bronze plan even if the Bronze premium looks cheaper on paper.

Verify your doctors and prescriptions are covered. Call your insurer or use their online provider directory before enrolling. Don’t assume.

Pro Tip: Watch for “embedded” vs. “aggregate” deductibles on family plans. With an embedded deductible, each family member has their own individual deductible. With an aggregate, the whole family shares one. This difference can dramatically change when your insurance actually starts paying.

Also check whether your plan uses a separate deductible for prescription drugs. Some plans apply drug costs to the main deductible; others have a standalone drug deductible that resets independently. Missing this detail is a common source of unexpected bills.

Revisiting your smart coverage guide each year during open enrollment is one of the simplest ways to avoid overpaying or being underinsured.

Our take: What most guides miss about health insurance terms

Most articles stop at definitions, and that’s a real problem. Knowing what a deductible is doesn’t tell you how it will feel three years from now when your health changes, your income shifts, or your family grows. The terms themselves are static, but your life isn’t.

We’ve seen families lock into a Bronze plan because the premium was low, only to face a $6,000 deductible after an unexpected surgery. We’ve also seen people overpay for Platinum coverage they barely used because they feared the unknown. Neither outcome is inevitable when you revisit your plan annually with fresh eyes.

The real insight is this: health insurance terms are not just vocabulary. They’re levers. Pulling the right ones at the right time, when your income changes, when you have a baby, when you start a new job, can mean thousands of dollars saved or protected. Coverage that matters most is coverage that fits your actual life, not just your enrollment-day assumptions.

Review your plan every year. Not just the premium. All of it.

Need help decoding your plan? We’re here.

Health insurance terms can feel like a puzzle with pieces that keep changing. Even after reading every guide, the real test comes when you’re comparing actual plans for your specific family, income, and health situation.

At Strawderman Financial, we help individuals and families across the United States make sense of their health insurance solutions without the guesswork. Whether you’re sorting through marketplace options, evaluating life insurance options alongside your health coverage, or just need someone to walk through your SBC with you, our advisors are here. Speak with an advisor today and get personalized guidance that could save your family real money.

Frequently asked questions

What is a deductible in health insurance?

A deductible is the amount you pay for covered healthcare services before your insurance starts to pay. For 2026, individual deductibles on ACA plans vary widely by tier, from near zero on Platinum to over $6,000 on many Bronze plans.

How do subsidies like Cost Sharing Reduction (CSR) work?

CSR lowers your out-of-pocket costs, including deductibles and copays, if you buy a Silver plan and earn between 100% and 250% of the federal poverty level. These Silver plan subsidies are applied automatically when you enroll through the marketplace.

What is the out-of-pocket maximum?

It’s the most you’ll pay in a year for covered in-network services before your insurer pays 100%. The 2026 ACA limit is $10,600 for individuals and $21,200 for families.

How do I know which plan tier is right for me?

Choose based on expected health costs: Bronze for lowest premiums if you’re generally healthy, Gold or Platinum if you need frequent care, and Silver if you qualify for subsidies through the marketplace.

Recommended

Comments